Overview of Current Ethanol Market: Prices, Production, Profitability, and Co-Products

|

|---|

|

Decision Innovation Solutions

3315 109th Street, Suite B

Urbandale, IA 50322

http://www.decision-innovation.com/

Ethanol Prices: Tumbling Gasoline Price with Ethanol Price

The U.S. ethanol industry will face several notable challenges in 2016, mainly low ethanol prices, high stocks, and a low production margin. The blending value of ethanol is largely correlated to the price of gasoline. As shown in Figure 1, the average rack price of ethanol in February 2016 was $1.46 per gallon and the average rack price of gasoline was $1.02 per gallon.

The average price of gasoline fell 17% from December 2015 to January 2016. From January to February, the average price of gasoline again dropped by 11%. For the same time period, the average price of ethanol dropped by 6% from December 2015 to January 2016 and increased by a slight 2% from January to February 2016.

As shown in Figure 1, there is a 44¢-per-gallon difference between the rack price of ethanol and that of gasoline in February 2016. This is the highest premium we have seen recently. Ethanol in general trades at a discount to regular gasoline, and this discount has been approximately 36¢ over the 2010-2014 period. The premium of ethanol over gasoline since November 2015 makes the blending economics unprofitable in the gasoline market.

We were curious about what type of statistical relationship occurs between Midwest ethanol rack prices and Midwest gasoline rack prices. We found that there is a positive correlation of 0.80 over the time period examined here. We also did a simple time series regression to find out the elasticity between Midwest ethanol and gasoline prices. Here the log values of average monthly ethanol rack prices are regressed upon the log values of gasoline rack prices in the Midwest from January 2010 to February 2016. We found that a 10% increase in Midwest gasoline prices brought about a 6.75% increase in Midwest ethanol prices.

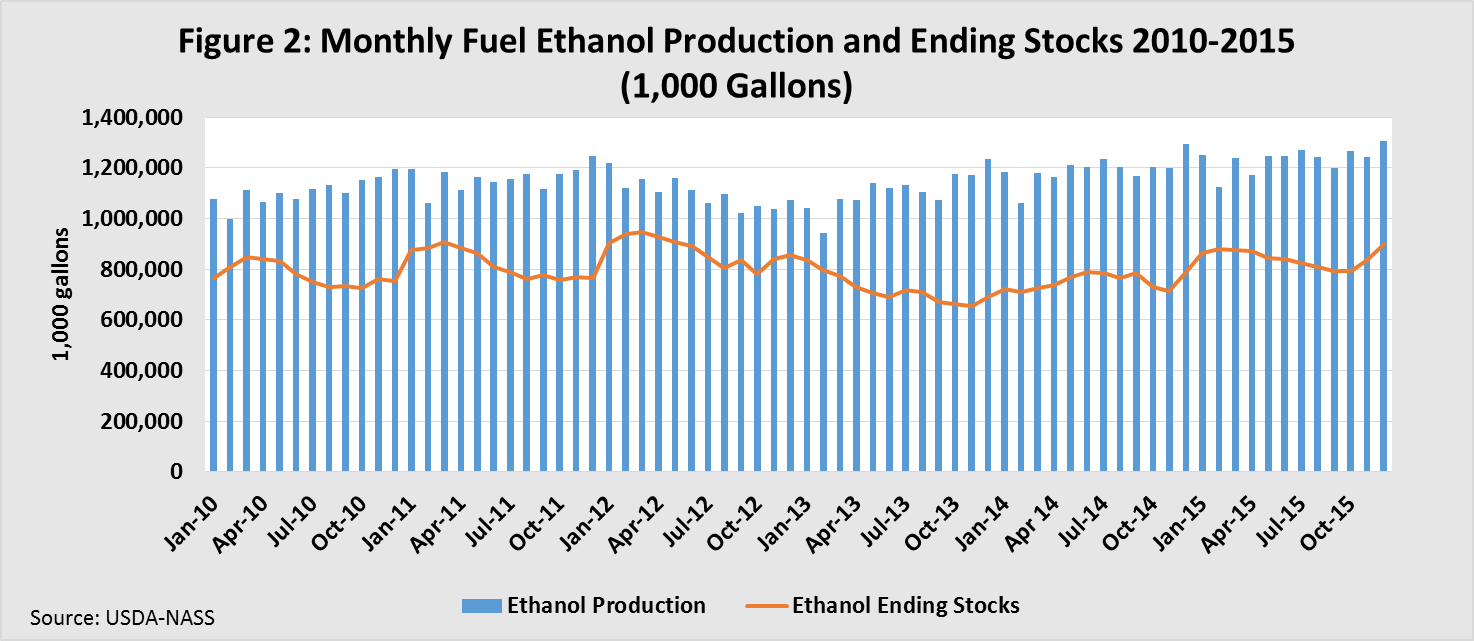

Production and Stocks: Surging Surplus Will Push Prices Down

U.S. ethanol production in February 2016 continued to surge, as production reached its highest level at 14.8 billion gallons in 2015 compared with 14.3 billion gallons in 2014 (see Figure 2). In addition, we saw an increase in ending stocks by the end of 2015. At the end of February 2016, U.S. fuel ethanol ending stocks were at 950 million gallons, up from 936 million gallons at the end of January 2016 and up from 904 million gallons one year ago. This is an increase of 5% from one year ago (EIA, 2016).

The ethanol production rate on average exceeded 980 barrels per day in both January and February 2016, as shown in Figure 3. This is well above the rate of production seen in January and February 2015. The weekly ethanol production exceeded one million barrels per day three times in 2015. This pushed stocks to an all-time high. But this happens when there is not enough domestic demand for ethanol, particularly during winter months when gasoline consumption is seasonally low. The industry is now looking for new demand from the export market.

Profitability: Outlook Is Not Encouraging

At the start of 2016, ethanol producers on average incurred a loss or broke even, as shown in Figure 4. In 2014, ethanol profits jumped to a record level of $1.31 per gallon, when crude oil prices were more than $100 per barrel. But in January 2016, the plummet in crude oil prices pushed the profits into negative margins. The profit margins began declining in May 2015, as we saw ethanol prices drifting down significantly along with crude oil prices. Margins currently remain a worry, with the medium to smaller plants experiencing losses and the larger plants at break-even levels.

In 2012, most of the ethanol producers in the Midwest survived the downturn and barely hung on when a widespread drought forced the shutdown of some plants with negative margins. Since the downturn in 2012, conditions have improved significantly, and the ethanol industry jumped to record profits in 2014.

Production margins are also being pressured by the comparatively higher price of corn, the main feedstock in U.S. ethanol production. Corn futures prices gained approximately 5% from the beginning of February 2016 compared with prices at the beginning of January 2016. In turn, the comparatively high regional corn prices have eroded the ethanol production margins.

Co-Product Market: Dried Distillers Grains with Solubles (DDGS) and Distillers Corn Oil (DCO)

The ethanol co-products market, in particular DDGS and DCO, is a very interesting market to follow because it’s a fairly new market. Also, this market is influenced by numerous factors, such as grain production, fuel, livestock, and exports.

Dried Distillers Grains with Solubles Market

There are few areas that the industry can be very optimistic about, especially the co-product market. Strong markets for DDGS and DCO have helped the ethanol industry tremendously at periods of low ethanol margins. A modern dry-mill ethanol plant produces approximately 2.8 gallons of ethanol, 0.66 pounds of DCO and more than 17 pounds of DDGS from a bushel of corn. The total production of DDGS in the 2014/15 marketing year was 36.1 million metric tons compared with 35.5 million metric tons in the 2013/14 marketing year, as shown in Figure 5. In general, DDGS contains 90% dry matter, 32% crude protein, and roughly 9% to 12% fat as an energy supplement. Therefore, DDGS has become a significant feed ingredient for livestock and poultry rations.

There has been strong export demand for DDGS, mainly from China and Mexico. Approximately 35% of total U.S. DDGS production has been exported in the past three years. China has been the key driver of the recent growth in the DDGS export market, and Mexico is the second largest importer.

In general, DDGS prices closely follow the price of corn, as shown in Figure 6. There is a positive correlation of 0.82 between the DDGS price from Iowa and the corn price in central Illinois from 2010 to 2016. Since DDGS has a different nutrient content than corn in livestock feed rations, the DDGS price can also be subject to the prices of other feed ingredients, mainly protein and energy substitutes. In order to account for that, we calculated a simple correlation coefficient between monthly average prices of DDGS and that of soybean meal and found that it’s 0.62 and relatively less associated than corn. Since 2010, the monthly average price of Iowa’s DDGS averaged 88% to the monthly average price of corn (Decatur, Ill) and 48% to the monthly average price of soybean meal (Iowa).

The cattle industry in the U.S. is the largest user of DDGS. One of the interesting points we should note here is that seasonality in cattle on feed numbers in the U.S. in a given year has reasonably good correlation with the seasonal price trend in DDGS.

In spite of the booming export market for DDGS, the outlook for 2016 is tentative and will mainly depend on Chinese trade policies. Last January, China officially filed anti-dumping and countervailing duties investigations with the World Trade Organization against U.S. DDGS exports to China. This kind of unwarranted trade restriction measure can disrupt exports and create uncertainty in the domestic ethanol market.

Distillers Corn Oil Market

DCO is produced at the majority of ethanol plants today. The DCO market was relatively small prior to 2000. However, the production of DCO has increased over the years, especially since 2008. The main markets for DCO are biodiesel plants, the animal feed industry, and the export market.

DCO’s role as a feedstock choice in the biodiesel industry has grown in the last five years. The U.S. Energy Information Administration (EIA) biodiesel production report published in February 2016 showed that approximately 1.044 billion pounds of DCO were used to produce biodiesel in 2015. Corn oil became the second most popular vegetable oil feedstock choice in the biodiesel industry in 2015, surpassing the usage of canola oil.

USDA reported that the DCO production was 1.391 million tons in 2015. As shown in Figure 7, 0.521 million tons were used in the biodiesel industry in 2015. That is approximately 37% of total DCO production in the U.S. during the last year. In addition to the biodiesel market, DCO has become a vegetable fat supplement to the livestock and poultry industry.

In addition to DDGS and DCO, there are other co-products that we have not discussed here or in previous editions. As reported by the USDA-NASS Grain Crushing and Co-Products Production 2015 Summary report in March 2016, corn germ meal, corn gluten feed, corn gluten meal, and edible corn oil are also important co-products produced at wet mill plants. We plan to look at those markets in future editions.

Concluding Remarks

The ethanol market will face a rocky road in the months to come, with instability among the small to medium-sized producers because of narrow margins. Overall profitability has shrunk to negative territory in February and March 2016 owing to higher stocks and lower ethanol prices following gasoline prices. This is not favorable for on-going struggles faced by the ethanol industry. DDGS prices may further weaken as the impending import ban from China will have a significantly negative impact on ethanol production.

Previous periods of negative ethanol margins were countered by strong markets for DDGS and DCO. That has not happened in the first quarter of 2016. However, the current DCO market is strong, as biodiesel production is ramping up in 2016 after the blenders tax credit was reinstated at the beginning of the year and a higher volume mandate of 1.9 billion gallons was approved, up from 1.8 billion gallons last year. The price of DCO at the spot market is trading at 30¢ to 32¢ per pound in Iowa compared with 24¢ to 26¢ per pound in January 2016. In addition to an increased demand from the biodiesel industry, the comparatively higher price of soybean oil has provided a much needed impetus to the DCO prices. The crude oil market is quite volatile, as OPEC and non-OPEC trade wars are beginning to complicate the clear market direction based on economic fundamentals.

Despite challenges, there are reasons to remain optimistic about the future of the ethanol industry. Currently the ethanol industry needs new demand, especially from export markets, to absorb historically high stocks and support prices. We have analyzed the export market for ethanol as well as DDGS in our second article in this April edition. We always look forward to your helpful comments and suggestions. Send them to sampath@decision-innovation.com

References

Decision Innovation Solutions, 2016, In-house data collection, Urbandale, Iowa.

EIA (U.S. Energy Information Administration), various, Weekly Ethanol Plant Production.

Monthly Biodiesel Production Reports

Hofstrand, D., and A. Johanns, 2015, Monthly Profitability of Biodiesel Production, Ag Marketing Resource Center:

Nebraska Ethanol Board, 2016, Ethanol and Unleaded Gasoline Average Rack Prices, Nebraska Energy Office, Lincoln, NE.

USDA-ERS (U.S. Department of Agriculture, Economic Research Service), 2015, U.S. Bioenergy Statistics.

USDA-NASS (U.S. Department of Agriculture, National Agricultural Statistics Service), 2016, Grain Crushing and Co-Products Production 2015 Summary, March 2016.