Corn, Ethanol and Crude Oil Price Relationships - Implications for the Biofuels Industry

AgMRC Renewable Energy Newsletter

August 2009

Robert Wisner

Robert Wisner

Professor of Economics and Energy Economist

Ag Marketing Resources Center

Iowa State University

rwwisner@iastate.edu

This article is a companion piece to a recent article that appeared in the AgMRC Renewable Fuels Newsletter by Dr. Dan O’Brien and Dr. Mike Woolverton from Kansas State University.(1) O’Brien and Woolverton quantify the recent relationships between ethanol and motor fuel prices and confirm that the corn market is closely related to the energy sector. In this article, we look at the evolution of these relationships over time and their implications for the future of the ethanol industry.

Corn’s Emergence as an Energy Crop

Rapid growth in corn processing for fuel ethanol has dramatically transformed Midwest crop-based agriculture in the last few years. It has transformed Midwest agriculture from a sector that experienced excess production capacity, low prices, and government income supports to a growth sector with frequent periods of tight supplies even with good crop yields.

Along with emerging government policies, a major uncertainty in the future growth and profitability of the corn-starch ethanol industry is the stability and strength of the corn-ethanol-crude oil price relationship. Ethanol production converts corn to a more valuable product, a motor fuel whose price is closely related to the major alternative, namely gasoline. The profitability of ethanol refineries depends heavily on the processing margin – the price of ethanol and DGS (distillers grains and solubles) minus the cost of corn and other expenses.

When ethanol was a much smaller industry, the ethanol sector could have a large annual percentage growth with only a minor impact on corn prices. That was the situation as recently as three to four years ago, when corn use for ethanol accounted for 12 to 14 percent of total U.S. corn use and prices were at or below government loan rates. But today, corn processing for ethanol is second in size only to the domestic feed market as a source of demand for corn.

| Corn processing for ethanol is second in size only to the domestic livestock feed market and may become the largest source of demand in three years. |

|---|

A sizeable increase in corn processing for ethanol now tends to strengthen corn prices much more significantly than in the past. Under current conditions, corn use for ethanol accounts for about 1/3 of the total demand for U.S. corn and is expected to account for an even greater share in the next few years with government mandates that call for increased ethanol use. Within three years, demand for corn for ethanol may well exceed the traditional largest source of demand for corn –livestock feeding. If the ethanol industry expands now and in the future, it may bid up corn prices – thus tending to narrow its processing margins unless ethanol prices simultaneously go up more than corn prices.

The relationship of corn prices to various fuel prices has major implications for crop and livestock farmers, the seed industry, grain elevators, food processors, suppliers of fertilizer, trucking firms, non-ethanol grain and oilseed processors, farm machinery manufacturers and dealers, railroads, livestock producers, agricultural lenders, and other businesses closely associated with the crop sector. The degree of stability and strength of the relationships has a major bearing on appropriate risk-management strategies as well as investment plans of these various firms.

The Evolution of Corn, Crude Oil, Gasoline and Ethanol Price Relationships

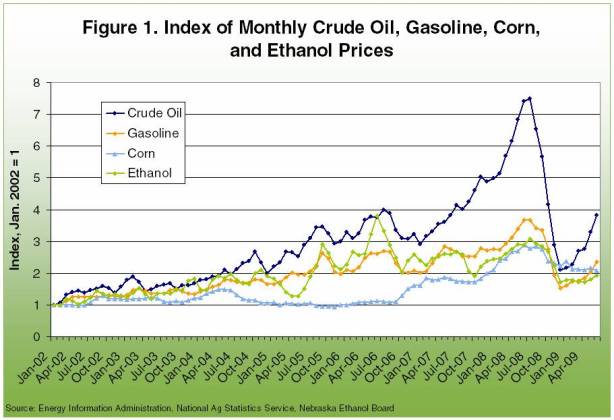

Figure 1 shows indices of corn, crude oil, ethanol, and gasoline prices since early 2002. The indices have a base of January 2002. Thus, the chart shows changes in prices of these commodities in comparable units since the base month. Prices shown are monthly nominal Nebraska wholesale ethanol and gasoline prices, Iowa corn prices, and the acquisition cost of crude oil at U.S. refining plants. An index of 2 would indicate prices are double those of January 2002.

Until early 2007, corn prices showed little relationship to crude oil prices. Since then, however, corn prices have been more responsive to changes in crude oil prices and have shown a close relationship to gasoline prices. The main reason for this is the growing importance of fuel ethanol as a percentage of total demand for U.S. corn. With the current large size of the ethanol industry, corn prices have become closely related to crude petroleum and gasoline prices because corn is now a major energy crop.

Perhaps surprisingly, crude oil prices increased percentage-wise much more than gasoline in 2007 and 2008. The difference can be partially explained by the fact that crude oil is not the only cost factor involved in producing gasoline. The production process involves a number of other costs that do not increase proportionately as crude oil prices rise.

Note also in Figure 1 that from late 2008 onward, corn and ethanol prices did not decline as sharply as crude oil and gasoline prices. For a few months, ethanol prices were above gasoline prices, thus reducing the incentive for blending ethanol with gasoline and tempering the demand for corn to be processed into ethanol. From March through June, ethanol prices increased only slightly despite a sharp increase in prices of both crude oil and gasoline. Failure of ethanol prices to move up with gasoline in part reflects the approaching blending wall as the average U.S. ethanol-gasoline blend nears 10%. (See our articles on the blending wall, and wild cards for ethanol.)

Note that since late 2007, the corn price index has closely followed changes in the ethanol price, although it remained above ethanol in the first half of 2009. Before that time, the relationship was almost non-existent. The close relationship since late 2007 reflects the ethanol industry’s very rapid growth and move up to a major share of the demand for corn. In the 2007-08 corn marketing year, ethanol accounted for about ¼ of the total demand for U.S. corn versus 19 and 14 percent respectively in the previous two years.

The Gasoline-Crude Oil Price Relationship

Figure 2 shows the approximate yield of various products from a barrel of oil. Non-fuel products include petrochemical feedstocks for products such as rubber, plastics, ink, crayons, bubble gum, dishwashing liquids, deodorant, eyeglasses, records, tires, ammonia, heart valves and many other items.(2) To calculate the gasoline price as a percentage of the gasoline equivalent of the crude oil price, we used the following formula: Gas price ($/gal.)/[crude oil price ($/barrel)x0.47]/ 19.7 gal./barrel. = gasoline price as a percent of gasoline’s share of the crude oil price in gasoline-equivalent gallons. Actual gasoline yields per barrel can vary some, depending on the type of crude being refined and market demand for gasoline vs. other petroleum-based products but this relationship should be a good approximation for examining the gasoline-crude oil price relationship.

Gasoline’s monthly share of equivalent crude oil prices since 1980 using this formula is shown in Figure 3. Gasoline’s share of crude oil prices has fluctuated widely over time and has declined in the last few years. Over this period, the high was in December 1998 when gasoline prices per gallon were 422% of the equivalent crude oil gallons. That contrasts sharply with a low of 133% in July 2008 and 140% in January 1981. A careful examination of the data did not identify a noticeable seasonal pattern in the gasoline share. However, the crude oil price line in Figure 3 suggests that gasoline’s share of the crude oil price varies inversely with crude oil prices. In other words, in times of rapidly rising crude oil prices, corn growers should expect gasoline prices to increase by a somewhat smaller percentage than crude oil. They also should be aware that even in times of relatively stable crude oil prices, gasoline’s share of the crude oil price can fluctuate widely. For example, in the 1986-2001 period of relatively stable crude oil prices, gasoline’s share of the crude oil equivalent cost per gallon fluctuated from 171% to 422%.

The Gasoline-Ethanol Price Relationship

Figure 4 shows a scatter diagram of the monthly index of ethanol and gasoline prices since January 2005. The straight line is a statistical regression of ethanol prices with gasoline prices. It shows the average relationship between the two series of price indices over this time period. The scatter of squares above and below the line indicates the two price series do not move with exact precision over time, although there is a strong relationship between the two markets.

In Figure 4, we have highlighted the dots for spring and early summer of 2005 and 2006. Both were times when ethanol prices deviated considerably from its normal relationship with gasoline prices.

This period of 2005 was a time when the ethanol industry was expanding very rapidly. For the 2005-06 marketing year, U.S ethanol production increased by 21% from the previous year. This also was a time when production capacity grew more rapidly than the infrastructure and markets for moving it to consumers. As a result, ethanol price increases lagged behind those of gasoline.

In the spring and early summer of 2006, an opposite situation occurred. Production of the oxygen enhancing additive for gasoline, MTBE, was halted due to concerns related to carcinogen issues. Since MTBE was the main alternative to ethanol for enhancing oxygen in reformulated gasoline, halting its production very quickly opened up a large new market for ethanol. The result was that ethanol prices moved well above gasoline prices for several months. That in turn accelerated the expansion in investments in new ethanol plants as well as infrastructure for delivering and marketing ethanol to final users. As production, transportation, and marketing capacities expanded, ethanol prices reverted back to a more normal relationship to gasoline. In May of 2009, ethanol prices were on the low side of their normal relationship with gasoline. This may reflect a U.S. average blend that is nearing the 10% “blending wall.”

Figure 5 provides an additional perspective on the relationship between gasoline and ethanol prices. The dark blue line is estimated from regression analysis of the relationship between ethanol prices and gasoline prices, excluding the extreme months in 2005 and 2006 noted above. In other words, regression-estimated ethanol prices are estimated based on their normal average relationship to gasoline prices from January 2005 through May 2009.

The orange line shows actual ethanol prices and provides a picture of how ethanol prices have deviated from their “normal” or average relationship with gasoline. As expected, the actual ethanol price line is more variable than the regression based line.

We have identified three periods when ethanol prices were lower than normal in relationship to gasoline. Each of these may have been a time when production capacity was expanding more rapidly than the market’s ability and/or willingness to absorb the product. The MTBE impact also is identified. The first half of 2009 is a period when ethanol prices have been lower than “normal” in relation to gasoline prices. This again may signal an approaching blending wall. As we have noted earlier and in previous articles, fuel ethanol has two markets, E-10 for conventional and flex-fuel vehicles and E-85 for flex-fuel vehicles only. The flex-fuel fleet is a very small percentage of the total U.S. gasoline-powered vehicles, and not all motorists want to use ethanol. For that reason, as the U.S. average ethanol-gasoline blend approaches 10%, as it is now doing, a “blending wall” begins to emerge. That limits the market for ethanol, thus tending to depress its price relative to gasoline. Unless the allowable blend for conventional vehicles is raised above 10%, ethanol prices in the future may move to an even lower percentage of their normal relationship to gasoline in the future. This would be the market’s way of attempting to encourage motorists that do not use ethanol to begin using the product. It would also be a signal to the ethanol industry to slow its expansion rate, thus slowing the expansion in demand for corn and tending to temper corn prices.

Corn and Ethanol Price Relationships

Figure 6 shows the relationship between ethanol prices and corn prices, expressed as indices with January 2002 having a value of one. We have highlighted the point for May 2009. For that month, corn has an index of 2.23 and ethanol has an index of 1.81. That means corn prices for the month of May 2009 were 2.23 times those of January 2002. Prices for ethanol were 1.81 times those of January 2002. The late spring and early summer of 2006, when MTBE production was halted shows on Figure 6 as a time of very high ethanol prices and low corn prices because ethanol refinery capacity was insufficient to respond to the surge in ethanol demand. The first half of 2005 was a period when ethanol prices were beginning to rise while corn prices remained low. July 2008 was a period of high prices for both corn and ethanol. For the first half of 2009, ethanol prices have been lower than “normal” relative to corn. As a result, ethanol processing margins have been very depressed (See our ethanol returns chart.) Corn prices were supported during that time by growing demand for ethanol, but also were strongly influenced in the short term by expectations about domestic and foreign crop production, commodity fund trading activity, currency exchange rates, and livestock feeding returns. While there is a longer term positive relationship between corn prices and ethanol prices, substantial short-term fluctuations around that relationship can occur. (3)

Summary and Implications

With rapid growth of the ethanol industry in the last few years, corn has become very much an energy crop as well as the world’s most important source of feed grains for production of livestock, poultry, and dairy products. This transition has created a strong but still somewhat variable relationship between corn prices and those for crude oil, gasoline, and ethanol. Ethanol, initially as an oxygen-enhancing additive and now also as a replacement for gasoline, has a price relationship with both crude oil and gasoline. That relationship has fluctuated in a moderate range in the past three years. At times when ethanol demand and prices have surged in the past, corn prices have tended to be strengthened. In opposite situations when ethanol production capacity has exceeded demand, ethanol prices have weakened relative to gasoline. That in turn has depressed ethanol processing margins, slowing the industry’s expansion rate and tending to temper corn demand growth and prices.

Ethanol production capacity is approaching a blend wall that is created by market limitations from a maximum ethanol-gasoline blend of E-10 for conventional U.S. vehicles. If this maximum blend is not raised substantially, we would expect ethanol prices to be more depressed in the future relative to crude oil and gasoline prices. That in turn has implications for owners of ethanol plants and investors in both starch-based and cellulose-based ethanol plants. It also has implications for corn and soybean growers, the livestock, poultry, and dairy industries, farm input manufacturers, the seed industry, grain elevators, the transportation sector, and other components of the Midwest economy.

Allowable ethanol-gasoline blending rates are not the only factor that will influence future crude oil, gasoline, ethanol, and corn price relationships. Another major element in the picture is greenhouse gas emissions regulations. Proposed California regulations, which may also be adopted by a number of other states if not nationally, favor ethanol produced from Brazilian sugar cane as well as non-agricultural alternatives such as compressed natural gas, compressed land-fill gas, hydrogen, and electric vehicles. (4)

If the maximum ethanol-gasoline blend for conventional gasoline-powered vehicles is not increased from 10%, we would expect ethanol prices to be depressed relative to gasoline.

References

1 O’Brien and Woolverton, Extension Agricultural Economists, Kansas State Research and Extension, The Relationship of Ethanol, Gasoline and Oil Prices, AgMRC Renewable Energy Newsletter, July 2009

2 Energy Information Agency, U.S. Department of Energy, “Frequently asked questions – Crude Oil”, 2008

3 O’Brien and Woolverton, Extension Agricultural Economists, Kansas State Research and Extension, The Relationship of Ethanol, Gasoline and Oil Prices, AgMRC Renewable Energy Newsletter, July 2009

4 Wisner, R., Biofuels and Greenhouse Gas Emissions on a Collision Course, AgMRC Renewable Energy Newsletter, June 2009 [] and Wisner, R., Wild Cards for the Ethanol Industry, AgMRC Renewable Energy Newsletter, July 2009

Data Sources

Energy Information Administration, U.S. Energy Department

Nebraska Energy Statistics, Ethanol

USDA, Agricultural Marketing Service

USDA, National Ag Statistics Service

Energy Information Administration, U.S. Department of Energy, “