Cellulosic Ethanol: Beyond the Kernel

By Sampath Jayasinghe

By Sampath Jayasinghe

Decision Innovation Solutions, 11107 Aurora Avenue, Urbandale, IA 50322

http://www.decision-innovation.com/

Cellulosic ethanol is ethanol fuel produced from agricultural residues such as corn stover (that is, the leftover stalk, cobs, leaves, and husks), switchgrass, wheat straw, or non-edible parts of plants. It gained much attention because its feedstock can be grown anywhere and can be sourced from agricultural crop residues. The U.S. Department of Agriculture (USDA) estimated that more than one billion tons of biomass feedstock are available for use in the United States annually (USDA, 2011). Corn starch from corn and sugars from sugarcane are the most common feedstocks for ethanol production. However, the production of cellulosic ethanol requires advanced technologies to break down cellulose into ethanol, unlike corn-based ethanol production occurring mostly in the United States and sugarcane-based ethanol production occurring mostly in Brazil.

Cellulosic ethanol is ethanol fuel produced from agricultural residues such as corn stover (that is, the leftover stalk, cobs, leaves, and husks), switchgrass, wheat straw, or non-edible parts of plants. It gained much attention because its feedstock can be grown anywhere and can be sourced from agricultural crop residues. The U.S. Department of Agriculture (USDA) estimated that more than one billion tons of biomass feedstock are available for use in the United States annually (USDA, 2011). Corn starch from corn and sugars from sugarcane are the most common feedstocks for ethanol production. However, the production of cellulosic ethanol requires advanced technologies to break down cellulose into ethanol, unlike corn-based ethanol production occurring mostly in the United States and sugarcane-based ethanol production occurring mostly in Brazil.

Plant material contains cellulose and hemicellulose in its cell walls, interconnected with lignin to support the rigidity of cell walls, so they are generally known as lignocellulosic materials in biotechnology. To produce ethanol from lignocellulose, first the cellulose and hemicellulose needs to be separated from the lignin using pretreatments and then hydrolysis using enzymes to make glucose and xylose. Then glucose and xylose are converted to ethanol by fermentation. All of these production steps create challenges to profitable yield of cellulosic ethanol per ton of biomass feedstock.

The first commercial-scale U.S. cellulosic ethanol plant was opened by POET-DSM Advanced Biofuels LLC in Emmetsburg, Iowa, in September 2014. This plant has the potential to utilize 770 tons of corn stover per day to produce 20 million gallons per year under the full capacity. Last October, the world’s largest cellulosic ethanol plant with capacity of 30 million gallons per year using corn stover was opened by DuPont in Nevada, Iowa. In addition, Quad County Corn Processors in Galva, Iowa, added cellulosic ethanol production in September 2014. The corn ethanol plant operates at 2 million gallons per year capacity based on corn kernel fiber technology, unlike POET and DuPont technology. Most of the cellulosic ethanol produced at these plants will likely be purchased by refiners and blenders in California to fulfill the state’s Low Carbon Fuel Standard (LCFS) program. More details about the LCFP program can be found in our May 2016 and June 2016 reports.

Cellulosic Ethanol Production

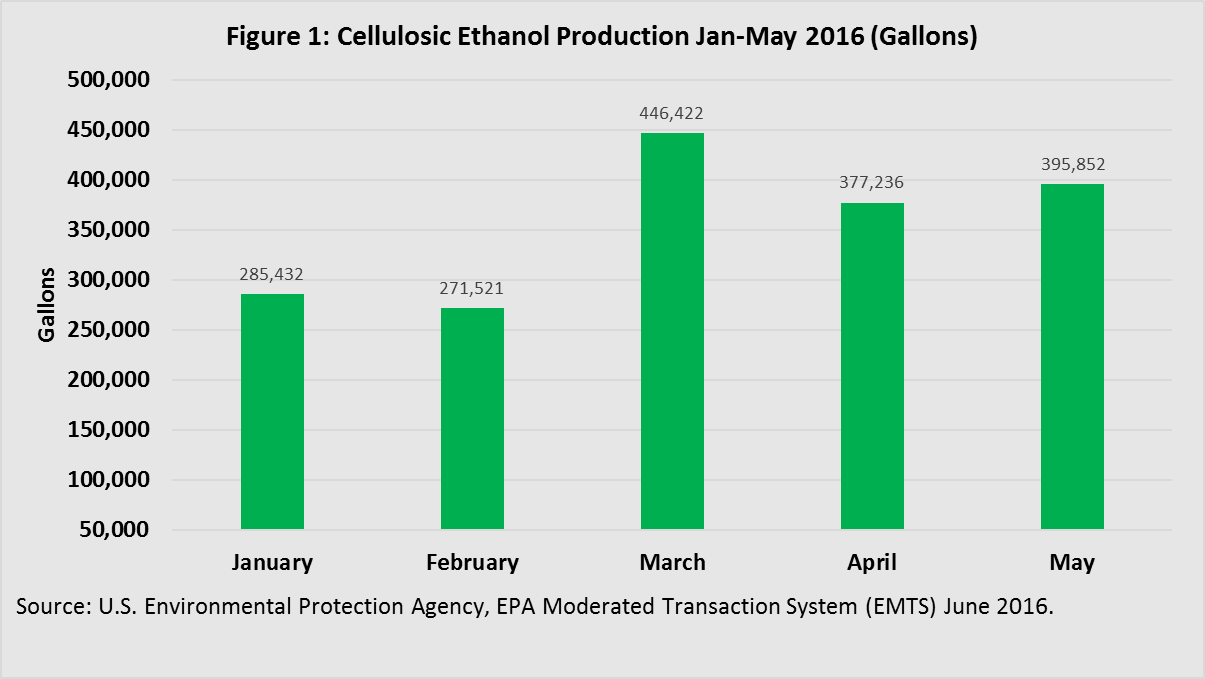

Commercial-scale cellulosic ethanol production has gained reasonable momentum during the first five months of 2016. Figure 1 shows the monthly production of cellulosic ethanol in 2016. In May 2016, the United States produced 395,852 gallons of cellulosic ethanol compared with 377,236 gallons in April, an increase of 5%. According to the Environmental Protection Agency’s (EPA) final ruling on the Renewable Fuel Standard (RFS) for 2016, the total cellulosic biofuel volumetric mandate is set at 230 million gallons. Cellulosic ethanol is one of three fuels included within the “cellulosic biofuels” category. The other two components of cellulosic biofuels include Renewable Compressed Natural Gas and Renewable Liquefied Natural Gas. For now, we are only addressing cellulosic ethanol.

As shown in Figure 2, the first ever qualifying production batch of cellulosic ethanol in the United States was 20,069 gallons in 2012, but there was no production reported in 2013. In 2014, the total production was 728,509 gallons.

Total production of cellulosic ethanol from January to May 2016 was 1.78 million gallons. The total production in 2015 was 2.18 million gallons, indicating that approximately 81% of the total 2015 production has been achieved in the first five months of 2016. Significant private and public investments over the last 10 years have underpinned this latest production level.

Cellulosic ethanol production has been significantly lower than expected since the national RFS was revised in 2010. This led the EPA to substantially reduce the required volume of cellulosic biofuels in its proposal for 2017 mandated renewable fuel published on May 18, 2016 (Renewable Fuel Standard Program: Standards for 2017 and Biomass-Based Diesel Volume for 2018). The total cellulosic biofuel volume is proposed at 312 million gallons for 2017. However, the statutory volume requirements for cellulosic biofuels for 2017 was set at 5.5 billion gallons according to the EPA’s RFS2. Year-to-date cellulosic ethanol production volume in 2016 is encouraging for cellulosic ethanol marketers, from the perspectives of both a national RFS and California’s LCFS program. Current production is proving to be a much needed impetus to promote growth in the cellulosic biofuel industry.

Cellulosic ethanol holds a few important selling points compared with corn-based ethanol and other renewable fuels. Cellulosic ethanol has the potential for lower life-cycle greenhouse gas (GHG) emissions compared with either corn ethanol or petroleum gasoline. Wang et al. (2012) estimated life-cycle energy consumption and GHG emissions from using ethanol produced from five feedstocks: corn, sugarcane, corn stover, switchgrass, and miscanthus. Compared to petroleum gasoline, Wang et al. (2012) found that ethanol from corn, sugarcane, corn stover, switchgrass, and miscanthus can reduce life-cycle GHG emissions by 19%–48%, 40%–62%, 90%–103%, 77%–97% and 101%–115%, respectively.

Another major attraction of cellulosic ethanol is the availability of feedstocks. Many of the alternative feedstocks can be grown on land that is considered less productive for conventional row crops. There are plenty of lignocellulosic biomass sources available in the United States but harvesting, transportation, and storage have been challenging because of many factors such as low material densities and moisture levels. Current research has been focused on the development of harvesting and transportation systems in order to improve biomass harvest field efficiency and reduce capital costs. Harvest capacity and transportation density are the two major limitations to biomass harvest and logistics.

Current estimates maintain that farmers can remove 1 ton of corn stover per acre, but sustainability has been the key issue. The question is how much biomass can be harvested sustainably from a corn field while still maintaining soil productivity? A USDA study indicates that corn stover harvest can be sustainable on corn fields with slopes of less than 3%, with consistent grain yield of at least 175 bushel per acre, and with good nutrient management plans having solid test records. This study also shows that nitrogen and phosphorus applications should not need to change, but potassium should be monitored at one ton per acre harvest rate.

Biomass Feedstock Prices

The economics of harvesting biomass feedstocks plays an important role in supplying continuous feedstock to cellulosic ethanol production. Farmers have a choice of whether they want to harvest the corn stover or not. A farmer’s stover profitability depends on the delivery price and the costs associated with harvesting and delivering corn stover.

USDA’s National Biomass Energy Report provides weekly prices of cornstalks, straw, and grass for Iowa, Minnesota, Nebraska, South Dakota, Kansas, and Missouri. Figure 3 shows the average monthly prices of all the reporting states from January 2014 to the first week of June 2016. The average May 2016 price of cornstalks was quoted as $32 per ton with a wide range of $21 to $40 per ton in the Midwest. In May 2016, cornstalks were priced at a discount to grass by $21 and to straw by $31 per ton on average.

A recent study by Khanna and Paulson (2016a) investigated costs associated with stover collection and the stover prices needed to cover the additional costs under different productivity, crop rotation, and tillage practice scenarios. The cost components are harvesting, baling, storage, and additional fertilization expenses to replace nutrients removed with the residue. The additional cost mainly depends on the stover yield which is determined by corn grain yield. Khanna and Paulson show that total production costs decline as the harvestable yield increases, indicating lower break-even stover prices. They also indicate, because of the potential higher removal rate in no-till lands, a larger percentage of corn stover can be harvested under the no-till practices compared with conventional tillage. With regard to crop rotation concerns, continuous corn results in lower stover yields because of lower grain yields and higher costs associated with stover removal on a per ton basis compared with a corn-soybean rotation.

In the second part of their study, Paulson and Khanna (2016b) show that the breakeven stover prices tend to be lower in areas with higher corn yield potential. This is because the amount of stover yield is expected to be related to corn grain yield. Corn-soybean rotation using no-till practices can be more profitable in stover harvesting than in rotation and tillage combinations given the price of stover.

The Future of Cellulosic Ethanol

Cellulosic ethanol under advanced biofuel policy still has a long way to go before realizing its statutory mandate after 10 years of RFS implementation. Development of advanced biorefinery technology to produce cellulosic ethanol took longer to come to fruition than what was anticipated in 2007. Even with the current seemingly viable production technology, the economics of producing cellulosic ethanol has remained unclear, underscoring an urgent need for further applied research, including understanding cellulosic ethanol yields per ton of biomass feedstock needed to make the fuel economically feasible while remaining ecologically sustainable. Other issues such as pre-processing/particle flow, dealing with field debris, and the high capital intensity of commercial production plants will continue to provide headwinds in the industry.

We have noticed news stories about DuPont agreeing to sell its products to Procter & Gamble for use in laundry detergent. There are also some cases in which cellulosic ethanol biorefineries are changing their production processes to make higher-value products, such as chemicals. While the potential for cellulosic ethanol appears to be enormous, a long-term, coherent policy is needed to improve efficiency, innovation, and sustainability before this potential can be realized.

Sources

Khanna, M., and N. Paulson, 2016. “To Harvest Stover or Not: Is It Worth It?" farmdoc daily (6):32, Department of Agricultural and Consumer Economics, University of Illinois at Urbana-Champaign.

Paulson, N., and M. Khanna, 2016. "To Harvest Stover or Not: Part 2." farmdoc daily (6):118, Department of Agricultural and Consumer Economics, University of Illinois at Urbana-Champaign.

U.S. Department of Energy, 2011. U.S. Billion-Ton Update: Biomass Supply for a Bioenergy and Bioproducts Industry. R.D. Perlack and B.J. Stokes (Leads), ORNL/TM-2011/224. Oak Ridge National Laboratory, Oak Ridge, TN. 227p. Published March 19, 2015.

Wang, M., et al., 2012. “Well-to-Wheels Energy Use and Greenhouse Gas Emissions of Ethanol from Corn, Sugarcane and Cellulosic Biomass for US Use.” Environ. Res. Lett. 7.